Knowledge and Insights

Are You Ready… For The New Nonprofit ASUs?

In our August 2018 newsletter, we highlighted the four new accounting standards updates (ASU) that will impact nonprofits in the next few years. ASU 2016-14, Presentation of Financial Statements of Not-for-Profit (NFP) Entities, will be effective for years ending December 31, 2018 and June 30, 2019. So now the question is, are you ready?

There are several provisions included in the ASU, from reporting expenses in functional categories and netting investment expenses with investment return to a new net asset classification with additional disclosure requirements. Though all those are important and have their own requirements, the one provision that nonprofits seem to have the most difficulty implementing is the liquidity and availability provision. This provision is aimed at improving the financial statement reader’s ability to assess the nonprofits’ liquidity and availability of resources. Readers should be able to determine that the organization has sufficient resources to meet financial obligations as they come due. By clearly showing restricted cash and equivalents, the new guidance should increase transparency in the financial statements and promote a thorough understanding of the nonprofit’s ability to fund operations.

The provision must be reflected both in narrative format and supported by financial information. First, a narrative about the nonprofit’s policies on managing funds to meet day-to-day cash needs for general expenditures within one year of the balance sheet date must be disclosed. Second, financial information about liquid assets that are available to meet general expenditures within one year of the balance sheet date must be shown. Availability of the assets may be impacted by the nature of the assets, external limits imposed by donors, contracts with others, and internal limits imposed by governing board decisions.

Depending on the size of your organization, you may present numbers in tables or charts or provide the required information in a few simple lines.

How can you present this in your financial statements?

- Classify assets and liabilities as current and noncurrent on the balance sheet.

- Sequence assets according to their proximity of conversion to cash and sequence liabilities according to proximity of their maturity and resulting use of cash.

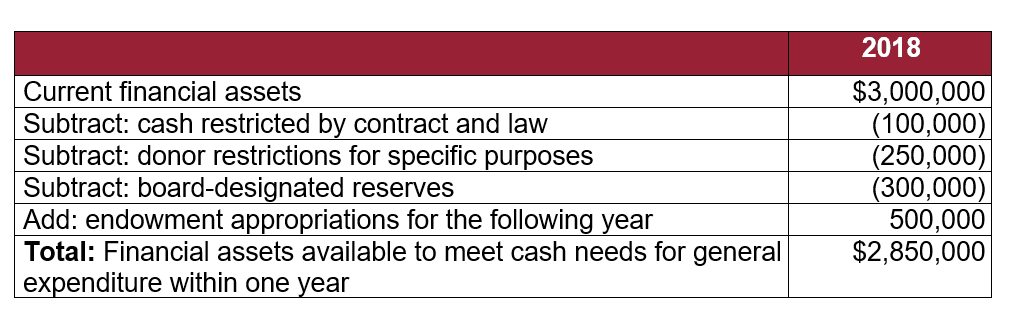

- Example of a disclosure to show availability of assets:

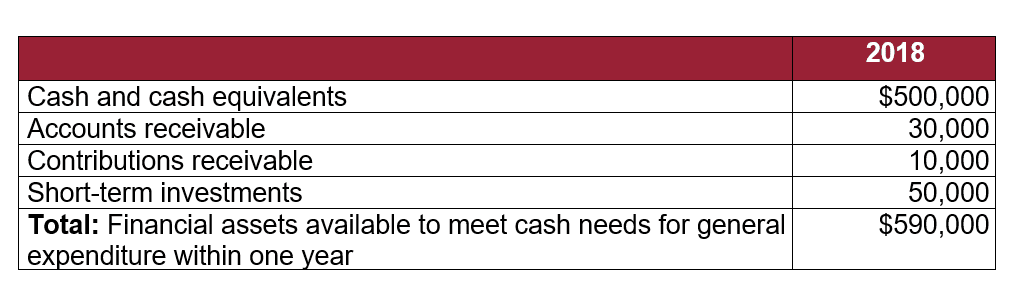

- Or maybe your financial statements are simple and you could present assets this way:

- Consider qualitative disclosures about the following:

- Responsibility of the NFP to maintain resources to meet donor restrictions, which may make those resources unavailable for general expenditure.

- Goals of the NFP for maintaining financial assets.

- Policies for investing excess cash.

- Policies for spending from board-designated endowment funds.

- Contractual agreements that make certain financial assets unavailable to fund general expenditures.

- Lines of credit that could be drawn down if the NFP did not have any liquid, available financial assets.

What does management need to consider?

- Consider the message that you wish to convey based on who will be reading the statements.

- Identify current procedures around board designations.

- Review current policies in place.

- Determine what level of financial assets your organization strives to maintain for daily requirements.

- Review or create a policy surrounding how cash in excess of daily requirements is handled.

- Know what resources are available for unanticipated needs.

What should management communicate to the board?

- Explain the disclosure requirements.

- Review and pass resolutions as necessary for board designations.

- Discuss anticipated costs for preparing disclosures, whether internally or externally.

We have created an implementation guide for each of the main provisions of ASU 2016-14, which includes detailed descriptions of the provisions, considerations for management and the board, as well as examples of disclosures. We also will hold an in-house seminar in January 2019. Keep a look out for our save-the-date emails. If you need assistance getting ready for the new ASUs, contact me at [email protected] or 609-689-2421, or reach out to a member of your Mercadien team.