Knowledge and Insights

How To Use & Optimize the Benefits from a Health Savings Account (HSA)

By:IsabelWhat is a health savings account (HSA)?

A health savings account (HSA) is a savings vehicle established to set aside funds tax free to pay for health care expenses. HSAs, created as part of the Medicare Prescription Drug and Modernization Act of 2003, allow individuals who have high-deductible health plans (HDHPs) to save money for health-care expenses tax free.

Who can establish an HSA?

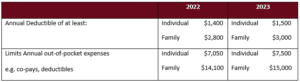

Generally, if you are covered under an HDHP, you are eligible to establish an HSA. A qualifying HDHP meets the following criteria:

You will not be eligible to open an HSA, even if you are covered under an HDHP, if any of the following apply:

- You are already covered under a non-HDHP, including a comprehensive major medical plan, a plan sponsored by your employer or your spouse’s employer, or a prescription drug plan or rider with a low deductible or no deductible. (Some health plans are exempted from this provision, including dental or vision care insurance, long-term care insurance, disability insurance, and accident insurance.)

- You can be claimed as a dependent on another person’s income tax return.

- You are entitled to Medicare coverage (i.e., you are age 65 or older), and have enrolled in Medicare.

Note: If your spouse has non-HDHP family coverage, but that plan does not cover you, you may still contribute to an HSA if you are otherwise eligible to do so. However, your spouse will not be eligible to contribute to an HSA.

How do you establish an HSA?

An HSA is a tax-exempt trust or custodial account that can be established through any qualified trustee or custodian, including a bank, an insurance company, or a third-party administrator. In some cases, this may be the same institution offering the HDHP. You can open an HSA on your own or, if available, through your employer. Employers may offer HSAs as part of a cafeteria plan.

Who can make contributions to an HSA?

You, your eligible family members, or others who wish to do so can make contributions to your HSA. If you’re employed, your employer may also make contributions to your HSA. Contributions may be made directly or through salary reduction under a cafeteria plan (if offered by your employer). However, no contributions can be made to your HSA once you retire.

How much can you contribute to an HSA?

You can choose to make monthly contributions to your HSA, or you can make a lump-sum contribution any time before your tax return becomes due (i.e., for most individuals, by April 15th of the year following the year for which contributions are being made), as long as your contributions have already accrued.

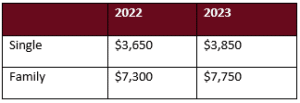

You may also be eligible to make additional “catch-up contributions” to your HSA if you are 55 or older. The catch-up contribution amount is $1,000. If eligible, both you and your spouse can make separate catch-up contributions to an HSA. However, no regular or catch-up contributions can be made once you reach age 65 and are enrolled in Medicare.

If you become eligible for an HSA after the beginning of the year your maximum contribution for the year is the annual maximum dollar amount for the year, even though you weren’t eligible for the entire year. However, you must remain in the HSA-eligible plan for the entire calendar year following the last month of the year in which you made that contribution. Otherwise, the contribution will be included in your gross income for the calendar year in which you ceased to be eligible and will be subject to an additional 20 percent penalty tax.

Can you make contributions to an HSA if you are covered under an FSA or HRA?

You may be ineligible to make contributions to an HSA if you are currently covered under a flexible spending account (FSA) or a health reimbursement arrangement (HRA) that duplicates coverage provided by the HSA. However, if you have an FSA or an HRA, you will be eligible to participate in an HSA if:

- Your FSA or HRA is a limited purpose account that repays or reimburses only vision, dental, or preventative care expenses

- Your FSA or HRA is a high-deductible arrangement (called a post-deductible arrangement by the IRS) that pays or reimburses health-care expenses only after the minimum annual HDHP deductible has been satisfied

- You suspend your HRA for a time by electing to forgo payment or reimbursement of HRA benefits incurred during the suspension period (your employer can continue to make contributions during the suspension)

- Your HRA is a retirement HRA that only reimburses medical expenses you incur once you retire (though contributions can be made before you retire).

Can your contributions earn interest?

Yes. As the account owner, you can direct your contributions to a savings or investment option offered by the qualified trustee or custodian of your HSA. Any interest and investment earnings on contributions grow tax deferred until withdrawn, and like contributions, will be tax free when withdrawn if used to pay qualified medical expenses.

How are contributions taxed?

Individual contributions you make to your HSA that do not exceed the maximum contribution limit are tax deductible on your federal income tax return. Because you deduct these contributions “above-the-line” when computing your adjusted gross income, you can deduct HSA contributions even if you don’t itemize. You can also deduct contributions made by a family member on your behalf.

If your employer makes contributions to your HSA, these are excludable from your gross income. Any contributions made through a cafeteria plan are treated as employer contributions. However, you cannot deduct employer contributions to your HSA.

How are distributions taxed?

You can withdraw money from your HSA for qualified medical expenses for yourself, your spouse, and your dependents. Distributions from an HSA for qualified medical expenses are not taxable. However, distributions for nonqualified expenses are considered taxable income and are subject to an additional 20 percent penalty tax.

What are qualified medical expenses?

Qualified medical expenses are health-care expenses, as defined by Internal Revenue Code 213(d), that are paid by you, your spouse, or your dependents. These include laboratory fees, prescription and nonprescription drugs, dental treatment, ambulance service, eyeglasses, and hearing aids, as well as many other health care expenses. HSA funds may also be used to cover health insurance deductibles and co-payments.

Generally, health insurance premiums, including HDHP premiums, are not qualified expenses, except for the following types of health coverage (1) COBRA coverage; (2) Qualified long-term care insurance (3) Health coverage maintained while receiving unemployment compensation and (4) Retiree health insurance other than a Medicare supplemental policy (Medigap).

What happens to funds remaining in your HSA?

At the end of the year

One of the advantages of HSAs is that HSAs do not have a “use it or lose it” provision. Funds remaining in your account at the end of the year are not forfeited and can continue to accumulate tax free year after year until withdrawn.

If you change jobs

An HSA is portable. Because the account is yours, you can keep it and continue to make contributions even if you change employers or leave the workforce.

If you divorce

If all or part of your interest is transferred to your spouse as part of a divorce settlement, it will not be considered a taxable transfer, and the transferred interest will continue to be treated as an HSA.

If you retire

Although you can no longer open or make contributions to an HSA once you reach age 65 and are enrolled in Medicare, you can take tax-free distributions from your account to pay for medical expenses. You can withdraw funds from your account for nonmedical purposes without owing a penalty (although the amount you withdraw will be subject to income tax).

If you die

Funds remaining in your HSA upon your death become the property of your designated beneficiary. If the beneficiary is your spouse, he or she becomes the account holder, and the account remains an HSA. If the beneficiary is not your spouse, the account ceases to be an HSA as of the day of your death, and the fair market value of the funds are includable in your beneficiary’s gross income.

Strategies to optimize the benefits

If you qualify to contribute to an HSA account, but do not need to use the funds currently to pay for your medical expenses, leave the funds grow tax deferred to maximize the benefit. You get the double benefit of a pre-tax contribution as well as tax deferred or tax-free distributions for qualified expenses. There is no required minimum distribution so you can let the funds grow as long as you like. Once you are over age 65, distributions can be spent on any purpose with no penalty, you only pay income tax if the distribution was not spent on qualified medical expenses.

Make gifts to eligible family members’ HSA accounts. While the gift counts toward the annual exclusion gift limit (2022 – 16,000; 2023 – 17,000), you are funding an account that will grow tax free until the funds are distributed and if spent on qualified medical expenses, the distribution is tax free.

If you are interested in learning more about the benefits of contributing to an HSA account or ways to maximize in the benefits of your HSA account, please reach out to me at [email protected] or 609-689-9700.