Knowledge and Insights

How Donor Advised Funds Can Maximize Tax Savings on Your Charitable Deduction Under the Tax Cuts & Jobs Act of 2017

By: Holly SaboThe Tax Cuts and Jobs Act of 2017 made significant changes to itemized deductions for individuals starting in 2018. While many are focused on the limitation of $10,000 of state and local taxes as a deduction, the tax benefit of your charitable contributions is also impacted. With the loss of most itemized deductions other than those listed below, many taxpayers will find themselves filing using the increased standard deduction.

2018 Allowable Itemized Deductions:

- a maximum of $10,000 in state and local taxes

- limited qualified mortgage interest

- investment interest expense

- medical expenses exceeding 7.5% of adjusted gross income

- federal disaster casualty losses

- charitable contributions (up to 60% of adjusted gross income for cash gifts to qualified charities)

2018 Standard Deduction:

- Single or Married Filing Separate – $12,000

- Head of Household – $18,000

- Married Filing Joint – $24,000

For those who do charitable gifting that have limited additional allowable deductions, a portion of the charitable deduction benefit will be lost in the process of climbing the standard deduction hurdle. Let’s look at an example of a married couple filing a joint return.

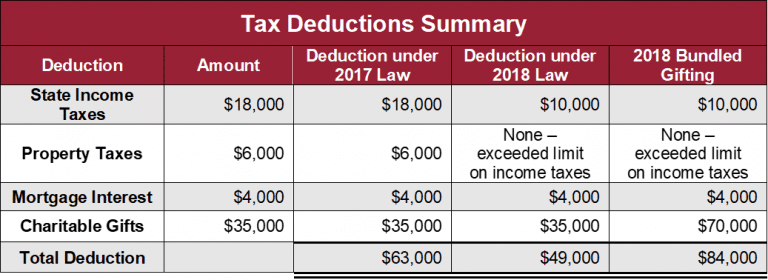

Ed and Mary are both employed and have one child. Their 2018 combined adjusted gross income is expected to be $380,000, which puts them in the 32% tax bracket. They own their home and have a mortgage on it. Their property taxes and mortgage interest expense are $6,000 and $4,000, respectively. They anticipate paying $18,000 in state income taxes. They usually give charitable gifts of $35,000 a year. Based on these facts, they would previously have had allowable itemized deductions of $63,000. Under the new tax law, their itemized deductions are $49,000. Their standard deduction would be $24,000 so they are only benefiting from $25,000 of their charitable gifting. They are saving $8,000 in taxes (32% of 25,000), which equates to a 22.86% savings.

If Ed and Mary “bundle” their charitable deduction by making two years’ worth of gifts in one year to a donor advised fund and make their usual gifts from the fund to the charities over years one and two, they increase the tax savings on the gift.

2018 – Bundled Gift

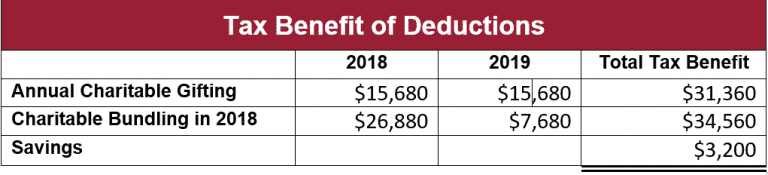

Charitable gift to donor advised fund of $70,000. Itemized deductions allowed increase by $35,000 of additional charitable gifting. The tax savings on the charitable gift are now $19,200 (32% of 60,000), which equates to a 27.4% savings.

2019 – No Gift

No charitable gifts directly by Ed and Mary; all gifts are paid out of the donor advised fund. Ed and Mary use the standard deduction since their deductions of taxes and mortgage interest only total $14,000.

2020 – Bundled Gift

Ed and Mary again contribute to the donor advised fund two or more years’ worth of charitable gifts and itemize on their tax return.

As you can see, with some planning, Ed and Mary are able to increase the tax savings on their gifting by bundling their gifts into one calendar year with the use of a donor advised fund, and yet still spread out the payments to the charities over two years. To learn more about donor advised funds, see our previous article here. If you think this strategy might be right for you, please contact me at [email protected] or 609-689-9700.

As you can see, with some planning, Ed and Mary are able to increase the tax savings on their gifting by bundling their gifts into one calendar year with the use of a donor advised fund, and yet still spread out the payments to the charities over two years. To learn more about donor advised funds, see our previous article here. If you think this strategy might be right for you, please contact me at [email protected] or 609-689-9700.